Learn more about President Biden's Executive Order on Safe, Secure, and Trustworthy Artificial Intelligence. ...

President Biden Signs Executive Order on Safe, Secure, and Trustworthy Artificial Intelligence

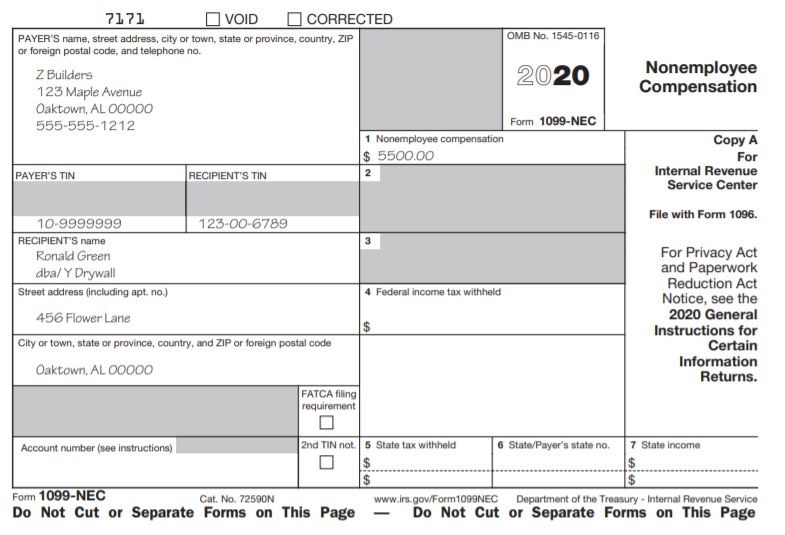

Starting in tax year 2020, the IRS is bringing back a form that hasn’t been used since 1982 – Form 1099-NEC.

This form will be used to report non-employee compensation. An image of what this form will look like is shown below.

From 1983 to 2019 non-employee compensation was included on Form 1099-MISC in box 7. However, it will now be reported in box 1 on Form 1099-NEC. Employers are required to file this form for any non-employee compensation paid to independent contractors of $600 or more and for non-employees who have provided services to the company. The amount reported should include payments for services and payments for parts or materials used to perform the services. A 1099-NEC can go to an individual, partnership, estate, or corporation. Some examples of independent contractors who might receive a 1099-NEC are attorneys, architects, and IT consultants amongst others.

One of the main reasons the IRS decided to bring back the 1099-NEC is because of the due date for non-employee compensation compared to all other payments. During the 2017 tax year, the IRS changed the filing deadlines for non-employee compensation to January 31, while all other payments were still due on February 28. By now creating a separate form, they are hoping to alleviate any confusion and complexities for employers.

Please contact your Schneider Downs tax advisor if you have any questions or would like to discuss the filing of Form 1099-NEC.

Learn more about President Biden's Executive Order on Safe, Secure, and Trustworthy Artificial Intelligence. ...

Learn more about the telemarketing scam and wire fraud charges against one of the "Real Housewives of Salt Lake City". ...

We’d love to hear from you. Drop us a note, and we’ll respond to you as quickly as possible.

Ask us

[email protected]

p:412.261.3644

f:412.261.4876

[email protected]

p:614.621.4060

f:614.621.4062

[email protected]

p:571.380.9003