Learn more about President Biden's Executive Order on Safe, Secure, and Trustworthy Artificial Intelligence. ...

President Biden Signs Executive Order on Safe, Secure, and Trustworthy Artificial Intelligence

There may come a day when a client, friend, or family member asks you what they can do when they owe the IRS and just can’t pay. You’ll want to be familiar with the installment payment plans that the IRS offers.

If a taxpayer has no other installment agreements with the IRS and is up-to-date on all required filings, he/she has a few options when it comes to making payment arrangements. The best option may be to use the IRS’s online payment agreement (OPA) system. If the amount owed is $50,000 or less and payment in full is made within 120 days, no set-up fees will be charged. Interest and late payment penalties will continue to accrue during the repayment time, but there will be no charge for the set-up fee. Note that payments must be made automatically via such means as direct debit, payroll deductions, etc.

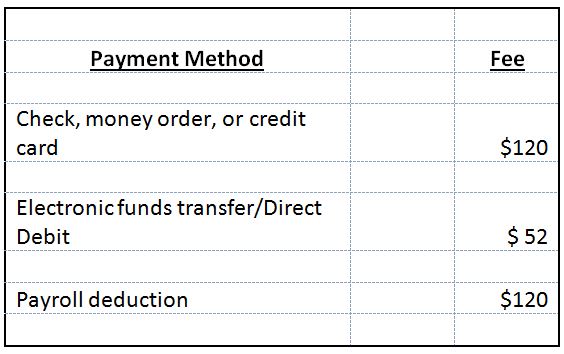

If the taxpayer knows that he/she cannot pay off the tax liability within 120 days, he/she can opt for the Streamlined Installment Agreement. Generally, the IRS will grant an installment repayment schedule of up to six years when the debt owed is $50,000 or less. The time period for repayment drops to three years when the debt owed is $10,000 or less. As with the 120-day repayment schedule discussed above, the taxpayer must be current on all other filings and recognize that interest and late payment penalties will accrue during the installment period. Fees for making this request are as follows:

When the OPA application cannot be used, the taxpayer making the request must complete the Form 9465, Installment Agreement Request. In most cases, the Form 9465 can be filed electronically.

If the taxpayer is opting to make payments by payroll deduction, another document, Form 2159, must be completed and attached. A portion is completed by the taxpayer, and a portion must be completed by his or her employer. Taxpayers opting for monthly payments to be made via payroll deduction cannot file Form 9465 electronically.

Finally, if a taxpayer owes more than $50,000, Form 433-F, Collection Information Statement, must also be filed.

With any of the installment payment options, the delinquent taxpayer is agreeing to:

Tax liabilities need to be dealt with. If the taxpayer has considered other alternatives that may be less costly, such as obtaining a bank loan, or using available credit on credit cards, and still cannot fully meet his or her debt, know that there are options. The IRS does want to work with taxpayers in order to collect delinquent taxes.

Learn more about President Biden's Executive Order on Safe, Secure, and Trustworthy Artificial Intelligence. ...

Learn more about the telemarketing scam and wire fraud charges against one of the "Real Housewives of Salt Lake City". ...

We’d love to hear from you. Drop us a note, and we’ll respond to you as quickly as possible.

Ask us

[email protected]

p:412.261.3644

f:412.261.4876

[email protected]

p:614.621.4060

f:614.621.4062

[email protected]

p:571.380.9003