Learn more about President Biden's Executive Order on Safe, Secure, and Trustworthy Artificial Intelligence. ...

President Biden Signs Executive Order on Safe, Secure, and Trustworthy Artificial Intelligence

Overview of the Refinancing Process

Refinance to Save on Financing Costs or Tap into Accrued Equity

Closing Costs are the Key Factor to Analyzing a Refinance

With the pullback in interest rates in 2020 given the monetary response to the COVID-19 virus, refinance activity was very robust. Individuals should always be cognizant of their financial liabilities and the associated interest rates on these obligations. While interest rates have ticked up since last year’s lows, historically, rates remain very low. In 2021, refinancing existing debt could still be a worthwhile option to consider for individuals seeking to lower their financing costs.

Refinancing debt is the process of revising or replacing an existing credit agreement with a financial institution. When individuals apply for debt refinancing, they are typically seeking more favorable terms such as a lower interest rate, a different loan term, or other key provisions. Consumer loans that are often considered for refinancing are mortgages, car loans, and student loans.

Desiring a lower interest rate is the most popular reason borrowers look to refinance debt. According to a March 2021 research note from Freddie Mac, a key player in the secondary mortgage market, because of mortgage rates touching historical lows in 2020, refinancing activity correspondingly reached its highest level since 2003.

When considering an individual’s refinance application for approval, financial institutions will re-evaluate one’s credit profile including credit score, the credit history (i.e. late payments), size and length of the loan, and employment and income history. Generally speaking, individuals are going to need a fair to good credit rating to be considered for most refinance programs.

The two most common refinancing scenarios are either to save money via a lower interest rate or a shorter term or a cash-out refinance.

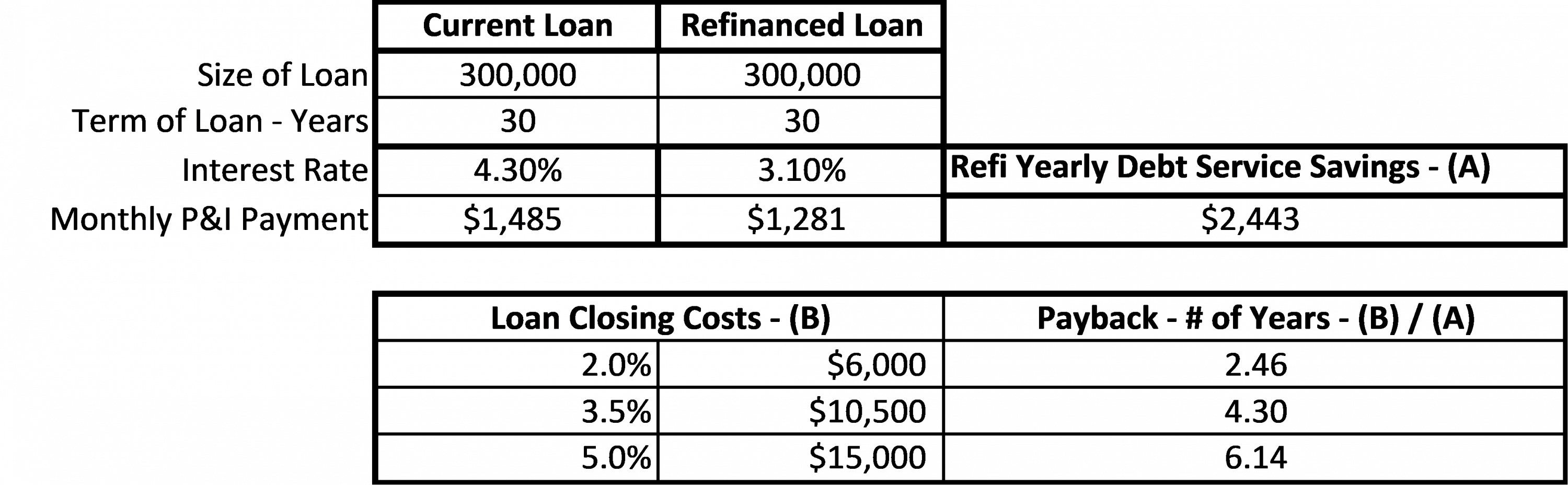

In the above-linked March report by Freddie Mac, borrowers who refinanced their 30-year fixed-rate mortgage to a new, lower interest rate, 30-year fixed-rate mortgage saved over $2,800 in annual mortgage payments by refinancing in 2020. The typical refinance loan in 2020 was a loan for about $300,000, with the borrower lowering their rate from 4.3% to 3.1%.

In addition to refinancing to a lower interest rate to save money, individuals also sometimes refinance shorter-term loans to save on interest costs over the life of the loan. When the difference between the interest rate on a 30-year fixed rate (currently 3.21% per Bankrate.com) and a 15-year fixed-rate mortgage (2.48% per Bankrate.com) widens, a refinance could be appealing.

According to Zillow, U.S. home prices increased almost 11% year-over-year in March 2021 with Zillow also projecting price increases of 10% over the next 12 months. For individuals seeking to tap into their home’s appreciation and associated equity (appraised market value less outstanding mortgage balance), a cash-out refinance could be an option. A cash-out refinance could be a source of capital for a home renovation, education costs, other investment opportunities, or an opportunity to consolidate debt to a lower interest rate (i.e. use the cash-out proceeds to pay off other higher-interest loans such as credit card or student debt).

In the event that a homeowner is considering a cash-out refinance, we would also suggest exploring a home equity line of credit given the potential lower closing costs.

As noted, when a consumer applies to refinance debt, the financial institution re-evaluates their creditworthiness and unfortunately, banks do not perform credit due diligence for free. According to Nerd Wallet, average closing costs can run between 2% and 5% of the loan amount, so on a $300,000 loan, closing costs could range from $6,000 to $15,000.

Given the significant amount of closing costs, it is imperative that individuals have a firm grasp on expected loan costs before proceeding with a refinance.

Assume an individual is considering a refinance of their existing 4.3% interest rate, $300,000, a 30-year fixed mortgage to a new 3.1%, $300,000, 30-year fixed mortgage. They would save about $204 per month from a lower principal and interest (P&I) monthly payment or $2,443 annually.

To evaluate whether refinance is beneficial, analyze the payback period of this refinanced loan (how many years until the lower annual debt service compensates for the upfront closing costs). Below, we illustrate the payback period for closing costs ranging from 2% to 5% of the loan.

As you can see, the payback period ranges from 2.5 to over 6 years depending on closing costs. Ultimately, the decision to or not to refinance is a personal decision factoring in how long the individual plans to live in that house, but the longer it takes to recoup the upfront closing costs should give individuals pause before proceeding with a loan refinance.

Should you be looking for ways to gain more control over your finances and liabilities, please contact Schneider Downs Wealth Management Advisors, LP. Our advisors would welcome a conversation with you.

Learn more about President Biden's Executive Order on Safe, Secure, and Trustworthy Artificial Intelligence. ...

Learn more about the telemarketing scam and wire fraud charges against one of the "Real Housewives of Salt Lake City". ...

We’d love to hear from you. Drop us a note, and we’ll respond to you as quickly as possible.

Ask us

[email protected]

p:412.261.3644

f:412.261.4876

[email protected]

p:614.621.4060

f:614.621.4062

[email protected]

p:571.380.9003