Learn more about President Biden's Executive Order on Safe, Secure, and Trustworthy Artificial Intelligence. ...

President Biden Signs Executive Order on Safe, Secure, and Trustworthy Artificial Intelligence

This article was originally published in Wedgewood Life magazine and is reprinted with their permission.

In our May article, we laid out some basic personal finance concepts including spending less than you make, pursuing a career you are passionate about, and discussing the long-term benefits of home ownership from a net-worth perspective. In addition, we highlighted the typical phases of lifetime wealth development starting with wealth creation, progressing to wealth accumulation, and ultimately the final stage of wealth distribution. This month we will focus on wealth creators.

We define wealth creators as individuals beginning to understand basic personal finance concepts and starting to establish personal wealth. Wealth creators are starting their careers, experiencing increased earnings potential, and trying to adhere to sound personal financial principles. When we work with wealth creators, we focus on the following planning items:

The other tangible benefit of establishing an initial baseline financial plan is the ability to reference it in the future when evaluating financial decisions such as how and where to invest additional excess cash flow as income levels increase, contemplating financing options for various expenses, and other financial decisions that will arise as one moves from wealth creation to accumulation.

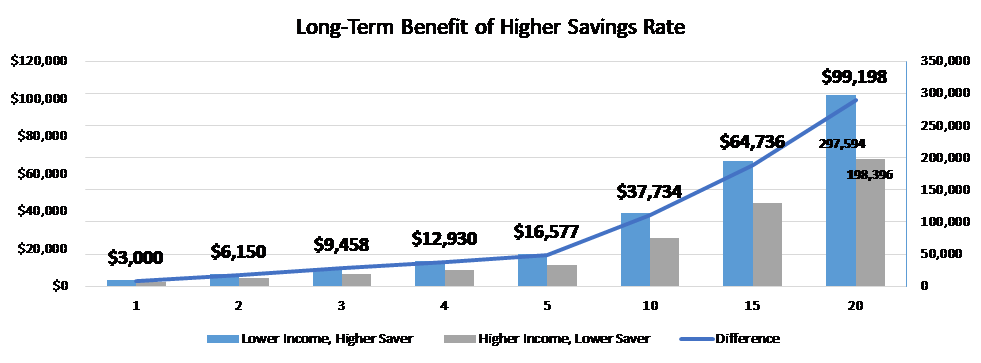

The chart below compares two individuals over a 20 year period – a lower income, higher saver earning $60,000 and saving 15% per year versus a higher income, lower saver making $120,000 and saving 5% per year.(This example assumed no wage inflation and a 5% rate of return.)

As you can see, the difference in the annual savings amount is $3,000 (15% of $60,000 versus 5% of $120,000). The aggregate investment balance between the two investors widens over time which is driven by the annual $3,000 savings difference combined with the power of compounding interest at an assumed 5% rate of return. At the end of this 20 year period, the lower income, higher saver has an ending investment balance roughly 1.5 times higher and almost $100,000 larger than the high income, lower saver.

In this example we kept the financial variables fairly simple.Although real-life variables will differ, the key concept remains the same – develop a personal financial discipline to increase your savings rate over time instead of spending income increases.The potential long-term financial benefits of an increased savings rate can be staggering. The continuous saving of excess cash flow paired with an investment rate of return is how a person evolves from wealth creator to wealth accumulator.

Material discussed is meant for informational purposes only, and it is not to be construed as investment, tax, or legal advice. Individual situations can vary, therefore, this information should be relied upon when coordinated with individual professional advice.

Learn more about President Biden's Executive Order on Safe, Secure, and Trustworthy Artificial Intelligence. ...

Learn more about the telemarketing scam and wire fraud charges against one of the "Real Housewives of Salt Lake City". ...

We’d love to hear from you. Drop us a note, and we’ll respond to you as quickly as possible.

Ask us

[email protected]

p:412.261.3644

f:412.261.4876

[email protected]

p:614.621.4060

f:614.621.4062

[email protected]

p:571.380.9003