Learn more about President Biden's Executive Order on Safe, Secure, and Trustworthy Artificial Intelligence. ...

President Biden Signs Executive Order on Safe, Secure, and Trustworthy Artificial Intelligence

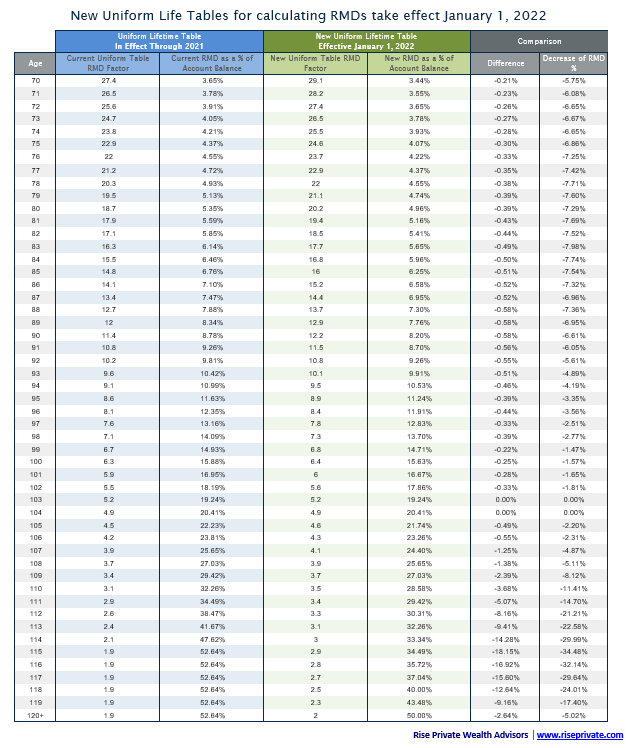

As of January 1, 2022, the updated Uniform Life Table for calculating a required minimum distribution (RMD) has now taken effect. To account for the overall increase in current life expectancy, RMD factors have increased, resulting in lower required distributions from tax-deferred accounts in 2022 relative to last year.

For illustration purposes, we’ll assume a 75-year-old individual has a $500,000 IRA balance. In 2021, their RMD on a $500,000 IRA with a RMD factor of 22.9 equates to 2021 RMD of $21,834. Compared to 2022, with the same $500,000 IRA balance, but updated RMD factor of 24.6, the RMD equates to $20,325, a 7% year-over-year reduction in the distribution. As one can see, the increased 2022 RMD factors result in incrementally lower required distributions. Readers will note that the penalty for not distributing one’s required minimum distribution is 50% on the amount of the distribution not taken.

Below you will find the updated Uniform Life Table showing the changes to the RMD factor, as well as differences between the new and old RMD tables. We have also provided some frequently asked questions regarding RMDs.

Should you have questions about required minimum distributions, retirement cash flow planning, or other financial planning considerations, please reach out to your trusted Schneider Downs Wealth Management Advisor. If you do not have an advisor, please contact us at [email protected].

A required minimum distribution is the minimum amount that you must withdraw from your tax-deferred retirement accounts each year beginning at a certain age. Examples of tax-deferred retirement accounts include, but are not limited to, Traditional IRAs, 401(k) accounts, or 403(b) accounts.

In recent years, the rules around the ages for taking RMDs have been adjusted. Initially, the rule for those who were born before July 1st, 1949 is that they begin taking distributions by April 1st of the year after they surpassed 70 ½. For those who were born after June 30th, 1949, a person must begin taking their RMD no later than April 1st of the year after you turn 72.

Schneider Downs Wealth Management Advisors, LP (SDWMA) is a registered investment adviser with the U.S. Securities and Exchange Commission (SEC). SDWMA provides fee-based investment management services and financial planning services, along with fee-based retirement advisory and consulting services. Material discussed is meant for informational purposes only, and it is not to be construed as investment, tax or legal advice. Please note that individual situations can vary. Therefore, this information should be relied upon when coordinated with individual professional advice. Registration with the SEC does not imply any level of skill or training.

Learn more about President Biden's Executive Order on Safe, Secure, and Trustworthy Artificial Intelligence. ...

Learn more about the telemarketing scam and wire fraud charges against one of the "Real Housewives of Salt Lake City". ...

We’d love to hear from you. Drop us a note, and we’ll respond to you as quickly as possible.

Ask us

[email protected]

p:412.261.3644

f:412.261.4876

[email protected]

p:614.621.4060

f:614.621.4062

[email protected]

p:571.380.9003